The cheapest way to send money to Dominican Republic is rarely the one with the lowest fee on the screen. Most providers show you a small transfer fee and then quietly take more on the exchange rate, where most Dominican families lose pesos without realizing it. This guide explains exactly how the real cost works, why providers can give you anywhere from 53 to 60 DOP for the same dollar, what the new 1% federal tax means for you, and how to compare your options in five minutes before sending. For the wider picture of every way to move money to your family in 2026, you can also read our complete guide to sending money to the Dominican Republic from the USA.

Why Exchange Rates Vary So Much Between Providers

The real cost of sending money has two parts. The first is the transfer fee shown on screen. The second is the exchange rate margin, which is the difference between the actual market rate and the rate the provider applies to your transfer. According to the World Bank’s Remittance Prices Worldwide database, the global average total cost of sending remittances is 6.36% of the amount sent, and the rate margin is usually a bigger part of that number than the fee. The same World Bank methodology notes that the exchange rate spread is “not quoted in the transfer fee,” which is why most senders never see it.

Why the variation is so wide between providers comes down to how the dollars become pesos. Every provider has to convert your US dollars into Dominican pesos somewhere along the path, and every layer of intermediation between you and your family adds a small margin. Old-school providers that rely on physical agents in the Dominican Republic stack three or four layers of intermediation: a wholesale FX desk, a settlement bank, an in-country agent, and a payout point. Each layer takes between half a percent and two percent. By the time the money reaches your aunt at the colmado, the spread can reach 6 to 8 percent above the real interbank rate.

Modern digital providers with direct relationships to Dominican banks and payment networks can compress those layers. Some compress them to almost zero. That is the difference between receiving 53 pesos per dollar and receiving 60.

Why ShareMoney’s Rate Is Consistently Competitive

ShareMoney is a brand of Omnex Group, a money transfer company founded in 1989 and headquartered in Englewood Cliffs, New Jersey. Omnex has been processing US-to-Dominican Republic remittances for more than two decades through a portfolio of heritage brands, and it operates under money transmitter licenses in 49 states with NMLS #899521. ShareMoney itself launched in 2014 as the digital, multi-corridor platform of the group.

What this matters for the rate you receive is simple. Three decades of operation in the corridor have built direct relationships with Dominican payment networks and established settlement infrastructure that newer providers cannot replicate quickly. ShareMoney does not need to add extra layers of intermediation because the relationships are already there. That is why, when you compare the cheapest way to send money to Dominican Republic in any given week, ShareMoney consistently lands among the top providers in the corridor by the amount of pesos your family receives.

This is not a marketing claim. It is the structural result of operating in the corridor for thirty-five years.

The 1% Federal Tax: Cash Costs You More in 2026

In 2026 there is a new line item in the cost of remittances that almost no one talks about. Under the One, Big, Beautiful Bill Act, the United States introduced a 1% federal excise tax on remittances effective January 1, 2026. The IRS confirms the rule applies to remittances funded with cash, money orders, cashier’s checks, or other similar physical instruments. Digital and electronic transfers are explicitly exempt, including transfers funded with debit cards or credit cards issued in the United States, ACH transfers from US bank accounts, and wire transfers through regulated financial institutions.

The practical consequence for Dominican families is concrete. If you walk into a Western Union or MoneyGram agent and pay in cash to send $500 to your family, the federal tax adds five dollars on top. Over a year of monthly remittances of that size, that is sixty dollars extracted from your family budget by the IRS. If you send the same $500 through a digital service like ShareMoney funded with your US debit card or bank account, the transfer is exempt and your family receives the full amount.

This single difference can outweigh the fee comparison most senders focus on, especially over a year of regular sending.

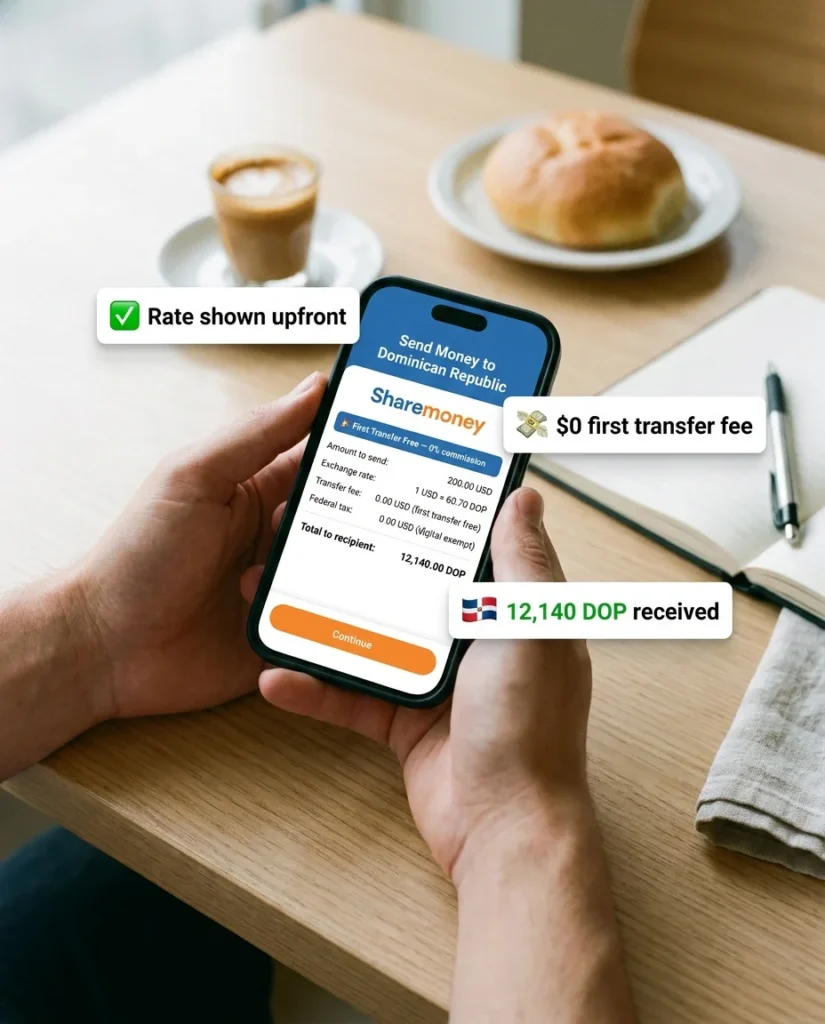

3 Fee-Free Transfers up to $500 Each

Beyond the structural cost advantages, ShareMoney offers a welcome promotion for new users. Your first three transfers to Dominican Republic have no transfer fee for amounts up to $500 each, paid with a US debit card. On your first transfer, the exchange rate applied is also preferential. The offer applies once per new user.

For a sender who tries the service with typical $300 to $500 transfers, the combination of no transfer fee on the first three sends, a preferential rate on the first, and the federal tax exemption means more of each dollar arrives as pesos during the welcome period.

How to Actually Compare Costs Before You Send

The fastest way to find the cheapest way to send money to Dominican Republic for your specific situation is to compare three or four providers head to head, with the same amount and the same payment method, before you tap send on any of them. The whole comparison takes about five minutes. Here is the method.

- Pick a fixed dollar amount you want to send. Use whatever you usually send. The classic test amounts are $200 and $500.

- Open three apps side by side. ShareMoney, plus two others you are considering. The most common comparisons in the corridor are with Remitly, Western Union, Xoom, and Sendwave.

- Enter the exact same amount in each app. Select the same destination (Dominican Republic) and the same delivery method. Bank deposit and cash pickup work differently, so compare bank deposit to bank deposit and cash pickup to cash pickup, never one to the other.

- Use the same payment method in each app. Debit card is the cleanest comparison because the fees are most consistent across providers. Credit card adds variable cash advance fees from your issuing bank that have nothing to do with the remittance provider.

- Look at the receive line. Every app shows you a line that reads “Your recipient receives X DOP” before you confirm. That number is the only number that matters. The fee shown above it is incomplete because it does not include the exchange rate margin.

- Take screenshots if you want to track over time. Rates change daily, so the cheapest way to send money to Dominican Republic this week might not be the same provider next week. The methodology stays the same.

If you want to understand exactly how the dollar-to-peso conversion is calculated and where the margin sits, our cluster article on the USD to DOP exchange rate breaks the mechanics down step by step.

Once you’ve compared the numbers, you can send money to the Dominican Republic with ShareMoney and see the exact fee and exchange rate before you confirm.

When ShareMoney Is NOT Your Best Option

A guide that claims one provider is always the cheapest way to send money to Dominican Republic for everyone is not telling you the truth. The corridor has real edge cases where ShareMoney is not the best fit, and being honest about them builds the trust that matters when you are sending hundreds of dollars across a border. Here are the situations where you should consider another option.

If your family in the Dominican Republic has a US dollar account at a Dominican bank and you want to send dollars rather than pesos, Wise operates with mid-market rates that may give you a marginally better outcome on USD-to-USD transfers. The catch is that USD accounts in the Dominican Republic are uncommon for families receiving regular remittances, so this case applies to a small minority of senders.

If your family lives in a small rural pueblo without a Caribe Express location, a BanReservas branch, or any of ShareMoney’s fifty-plus payout partners, a Western Union or MoneyGram agent network may simply offer physical coverage that the digital path does not reach. Coverage trumps price when there is no alternative.

If your family is already comfortable using a specific app and the savings difference is small, the cost of asking them to learn a new flow may exceed the savings. Trust and ease in the receiving end are real costs, even if they do not show on a fee screen.

For everyone else, which is most Dominican families sending from the USA, the structural advantages we covered above usually make ShareMoney the cheapest or near-cheapest option that delivers the most pesos for each dollar.

Frequently Asked Questions

Why are some providers’ rates so much worse than others?

Because each layer of intermediation between the dollar you send and the peso your family receives adds a margin. Providers with direct banking relationships in the Dominican Republic compress those layers. Providers that route through physical agent networks add more layers and more margin.

How do the 3 fee-free transfers work?

Your first three transfers have no transfer fee for amounts up to $500 each, paid with a US debit card. The preferential exchange rate applies to the first transfer only. The offer applies once per new user and does not combine with other promotions.

Does the 1% federal tax really not apply to ShareMoney?

The 1% excise tax established by the One, Big, Beautiful Bill Act applies to remittances funded with cash, money orders, or cashier’s checks. ShareMoney transfers funded with US debit cards, US credit cards, ACH bank transfers, or US-issued prepaid cards are exempt under the IRS rule.

What’s the difference between fee and exchange rate margin?

The fee is the transparent number shown on the app before you send. The exchange rate margin is the difference between the actual interbank rate (mid-market) and the rate the provider applies to your transfer. The margin is usually larger than the fee, and most providers do not show it as a separate line.

How often does the exchange rate change?

Daily, sometimes intraday. The Dominican peso trades in a managed-float regime against the US dollar, and providers update their rates throughout the business day. The cheapest way to send money to Dominican Republic this week might not be the cheapest next week, which is why the comparison method above matters more than any single ranking.

Get the cheapest way to send money to Dominican Republic with ShareMoney

What does not change is what your family needs. The grocery bill at the colmado. School fees in San Pedro. The medication your tía has been postponing. ShareMoney makes sure that every dollar you send arrives at its destination at a rate that is consistently competitive in the corridor, with the federal tax exemption built in, and with no transfer fee on your first three transfers up to $500 each. After those, the cost is small and visible before you confirm. Download the app and compare for yourself.

Related reading: Send Money to the Dominican Republic from the USA: Best 2026 Guide · Send Money to BanReservas from the USA: The Best Guide for Dominican Families