Getting the best exchange rate when sending money from the USA can mean the difference between your family receiving $480 or $450 on a single transfer. People in the United States sent nearly $80 billion abroad in 2023, according to World Bank data. Behind that number are millions of families where one person works here and another is counting on what gets sent home each month. If you are one of them, the exchange rate is not a detail. It is the difference between your family receiving $480 or $450 when you send $500.

Most people focus on the transfer fee. The fee is visible, listed at checkout. The exchange rate markup is quieter. Banks and some traditional services build a margin into the rate itself, and it adds up far faster than any flat fee does.

This guide explains what you need to know to get the best exchange rate when sending money from the USA, how exchange rates actually work in a transfer, what to watch for, and how to make sure every dollar you send goes as far as possible.

What an Exchange Rate Actually Means for Your Transfer

The mid-market rate is the “real” exchange rate. It is the one you see on Google or XE.com, the rate at which banks trade currencies between themselves. No one sends money at exactly that rate, but it is your baseline. The closer your provider gets to it, the better the deal for you.

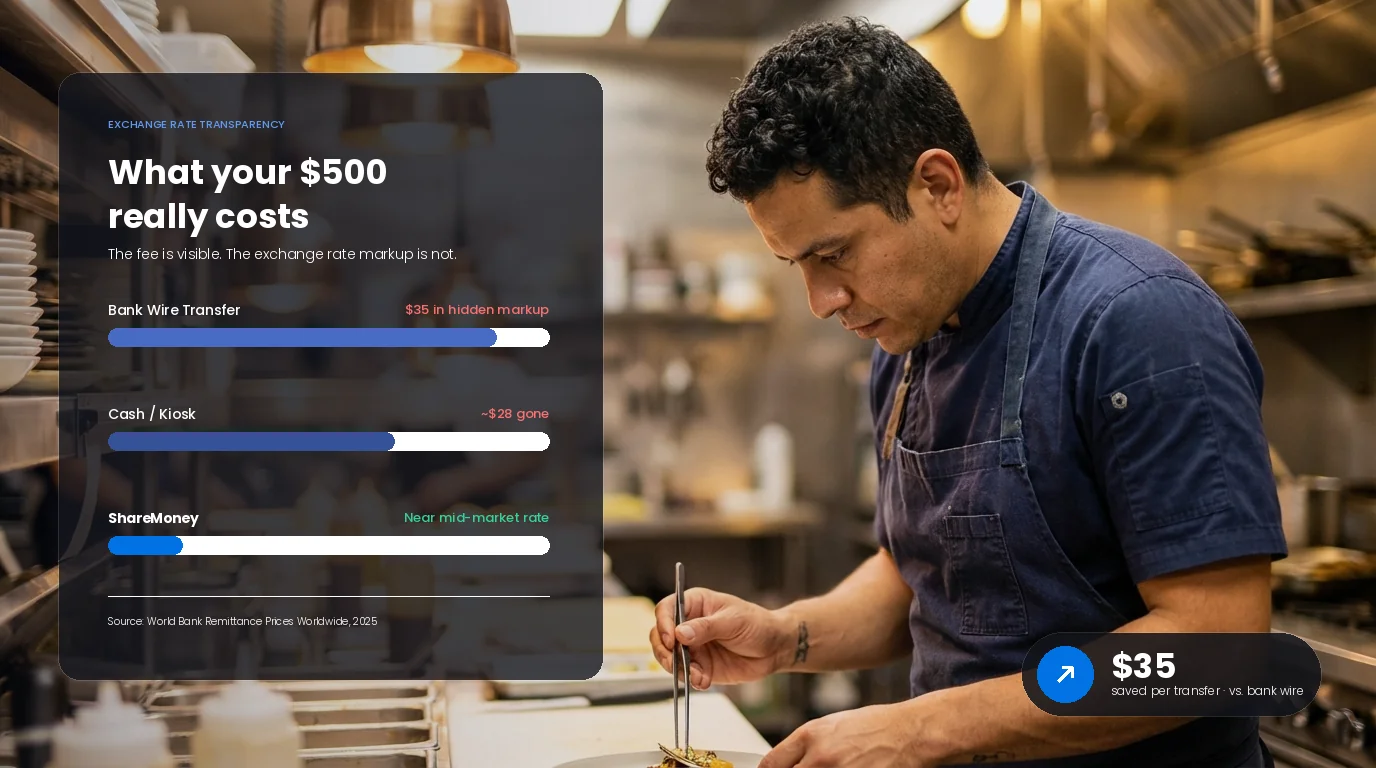

When a bank or transfer service applies a markup, they shift the rate in their favor. They might quote you 16.80 pesos per dollar when the mid-market rate is 17.40. That 3.5% difference is silent revenue for them. On a $500 transfer, that is $17.50 your family does not receive. Over 12 months of monthly transfers, it is $210 lost to a rate no one told you about clearly.

Digital remittance apps tend to offer rates much closer to mid-market than banks or physical exchange kiosks. According to World Bank data, the average total cost for a $200 transfer is around 6.5% globally in 2025. Digital providers average closer to 5%, while traditional methods including bank wire transfers hit 7% or more. Some bank-specific corridors reach as high as 17%.

The gap matters most for the people who send the most frequently.

Banks, Kiosks, and Apps: Where Your Money Actually Goes

Your bank is usually the most expensive way to send money internationally. Banks charge a transfer fee (often $25 to $50) and apply an exchange rate that includes a hidden markup of 3 to 5 percentage points above mid-market. Wire transfers also arrive slowly, typically 3 to 5 business days.

Currency exchange kiosks (airports, malls, exchange bureaus) are designed for travelers converting physical cash. They are not built for remittances. Their exchange rates are often the worst available, and they operate on physical cash, which creates an additional problem in 2026 that did not exist before.

Digital remittance apps like ShareMoney are built specifically for international transfers. They show you the exchange rate upfront before you confirm, charge lower flat fees, and process transfers faster, often within minutes for bank deposit and cash pickup.

To put numbers on it: if you send $1,000 to Mexico through your bank at a 5% exchange rate markup plus a $35 wire fee, your family receives the equivalent of roughly $915 in purchasing power. Through a digital app at a 1.5% markup and a small flat fee, they receive closer to $975 or more. That is not a rounding error. For families who send regularly, it adds up fast.

The 2026 Remittance Tax: Why Your Debit Card Matters More Than Ever

Starting January 1, 2026, a 1% federal excise tax (under IRC Section 4475) applies to certain international money transfers from the United States. This is not a rumor. It is in effect now.

Here is the part most people do not know yet: the tax only applies to transfers paid with cash. That includes cash handed over at a Western Union or MoneyGram counter, money orders, and cashier’s checks.

Transfers made with a debit card, credit card, or bank account are fully exempt.

What this means in practice: if you send $1,000 to the Dominican Republic at a cash window, you pay $1,000 plus the 1% tax ($10) plus whatever fee the agent charges. Total cost is $1,025 or more before the exchange rate even enters the picture.

If you send that same $1,000 through ShareMoney using your debit card, there is no 1% tax. For new users, the first transfer is free. For returning users, the fee is transparent and shown before you confirm.

The 1% may not sound like much in isolation, but combined with worse exchange rates at physical locations and a per-transaction fee on top, cash transfers now cost significantly more than digital ones. For a family that sends $500 twice a month, the difference over a year can exceed $200.

How to Read a Transfer Quote Before You Send

Any reputable service will show you the full cost before you confirm. Here is what to check:

Rate vs. mid-market. Search “USD to MXN” or “USD to DOP” on Google and compare it to what the service shows you. If the offered rate is more than 2 percentage points below mid-market, you are paying a hidden markup on top of any stated fee.

The fee. Some services charge a flat fee per transfer. Others build everything into the rate and advertise “zero fees.” Neither is automatically better. Total the real cost: what you send minus what your family receives, divided by what you sent. That is your actual cost percentage.

Delivery method. Bank deposit and cash pickup at partner locations often have different rates and fees. Faster delivery sometimes costs more, but not always. Check both before you decide.

Delivery time. In emergencies, speed matters. Transfers through ShareMoney to most destinations arrive within minutes. That is useful to know before you are in a situation where it matters.

Sending by Corridor: What to Expect

Exchange rates fluctuate daily. There is no fixed number that is always right. But here is what you can expect from well-structured digital transfers:

Mexico. The USD to MXN rate changes daily, but digital apps consistently land 2 to 4 percentage points above what banks offer. Cash pickup is available at OXXO, 7-Eleven, Walmart, Elektra, Farmacias Guadalajara, Soriana, HEB, and more than 30,000 additional locations across Mexico. Bank deposit is also available. Read the full guide to sending money to Mexico.

Dominican Republic. The DOP rate is subject to local Central Bank policy. Digital transfers via ShareMoney include cash pickup through Caribe Express and bank deposit to Banco Popular, Banco BHD, Banco Reservas, and other local banks. Full guide to sending money to the Dominican Republic.

Pakistan. The PKR has seen significant fluctuation in recent years. Digital transfers allow for faster locking of a rate. ShareMoney supports bank deposit to all major Pakistani banks. Full guide to sending money to Pakistan.

Five Things That Cost You More Than You Realize

- Bank wire transfers. The combination of a $35 fee plus a 4 to 5% exchange rate markup is standard at major US banks. On a $500 transfer, that is $55 or more gone before your family receives anything.

- Cash at a physical agent. As of January 2026, cash transfers carry the 1% federal tax on top of the agent fee and whatever exchange rate that location applies. Three costs stacked, none of them small.

- Sending in small, frequent amounts. If you pay a flat fee per transfer, sending $200 four times costs four times the fee. Consolidating when possible reduces total fee exposure, though you need to weigh that against urgency.

- Not checking the mid-market rate first. It takes 30 seconds on Google. Knowing the real rate before you open a transfer app tells you immediately whether the service is offering a fair deal or building a margin into the rate.

- Ignoring the delivery method. Bank deposit is often faster and cheaper than cash pickup for some corridors. Cash pickup can be faster in others. The right choice depends on your family’s situation and the specific country.

How ShareMoney Helps You Get the Best Exchange Rate When Sending Money from the USA

ShareMoney is a digital remittance app operated by Omnex Group (NMLS #899521), a company with over 30 years of experience processing international transfers. The app is available on iOS and Android.

To send money, you enter the amount, choose the destination country and delivery method, and ShareMoney shows you the exact rate and fee before you confirm. Nothing changes after you tap send. The rate shown is the rate applied.

You can pay by debit card (Visa or Mastercard), credit card (Visa or Mastercard), or bank account (ACH). All three are exempt from the 2026 remittance tax.

For new users, the first transfer is free: zero commission and a preferential exchange rate above the standard rate, applicable on transfers up to $500 with a debit card.

ShareMoney covers more than 75 countries across Latin America, Asia, and West Africa, with over 175,000 cash pickup locations globally and 24/7 customer support in English, Spanish, Vietnamese, Portuguese, and French.

Frequently Asked Questions

What is the best way to get a good exchange rate for international transfers?

The best exchange rate when sending money from the USA comes from digital remittance apps that show the full rate and fee upfront before you confirm. Compare the offered rate to the mid-market rate (available on Google or XE.com). A difference of 1 to 2 percentage points is reasonable for most apps. More than that, and you are paying a hidden markup.

Does the 1% remittance tax affect my ShareMoney transfers?

No. The 1% federal tax (effective January 2026) applies only to transfers paid with cash. ShareMoney transfers are made by debit card, credit card, or bank account, all of which are exempt.

How do I know if my bank is giving me a bad exchange rate?

Check the mid-market rate on Google for your currency pair (for example, “USD to MXN today”). Then compare it to what your bank shows you in their wire transfer tool. If the rate your bank offers is more than 3 percentage points below mid-market, you are losing more to the exchange rate than to any stated fee.

Does the exchange rate change while my transfer is processing?

With ShareMoney, the rate shown at the time you confirm is the rate applied to your transfer. You are not exposed to rate movements between confirmation and delivery.

Is the first transfer really free?

Yes. For new users, the first transfer carries no commission and includes a preferential exchange rate. Applies to transfers up to $500 sent by debit card. The offer cannot be combined with other promotions.

What countries does ShareMoney cover?

More than 75 countries, including Mexico, Dominican Republic, Colombia, Brazil, Guatemala, El Salvador, Ecuador, Peru, the Philippines, Vietnam, Pakistan, Nigeria, Ghana, Senegal, and many others across Latin America, Asia, and West Africa.

Send Smarter. Your Family Receives More.

What you want from an exchange rate is simple: the number your family sees when the money arrives. The fees, the markups, the taxes are just friction between your paycheck and that number. The less friction, the better.

ShareMoney was built to help you get the best exchange rate when sending money from the USA, every time. Download the app and start your first transfer free.