Sending money to Mexico looks like a transaction. The Western Union receipt in your wallet, the screenshot of the BBVA confirmation on your phone, the $400 you sent on Tuesday so your mom could pay the doctor on Wednesday: these are not transactions. They are a thread. And that thread is what holds together the largest diaspora in the United States, more than 38 million people of Mexican origin, who in 2024 alone sent $62.5 billion home. According to BBVA Research, that single corridor (USA to Mexico) made up 96.6% of every dollar Mexico received in remittances last year.

Sending money to Mexico is the most common act of long-distance love in the Americas. And yet, almost no one talks about what it really means. This is that conversation.

The Number Behind the Number

$62.5 billion is a difficult figure to picture. It is more than the entire GDP of Honduras. It is more than what Mexico earns from oil exports in some quarters. It is 3.4% of Mexico’s GDP, the same share that public education takes from the federal budget. And it arrived in Mexico the way it always arrives: in pieces. In 13.7 million separate transactions. In an average of $393 per transfer. In texts that say “ya te llegó, mamá” sent at 9 p.m. from a kitchen in Riverside, a delivery van in Houston, a hospital break room in Chicago.

One out of every three of those dollars came from California. Another 15% came from Texas. Together, those two states account for almost half of every peso that crossed the border last year. The other half is spread across Illinois, Arizona, Georgia, North Carolina, New York, and a hundred smaller communities where the Mexican-origin population has quietly become a structural part of local life: the framer in Atlanta, the line cook in Nashville, the certified nursing assistant in Charlotte, the sous chef in Seattle. People whose names rarely appear in remittance reports, but whose paychecks fund three-quarters of the rural economy of Michoacán.

Three Mexican states receive most of what gets sent: Guanajuato (8.9%), Michoacán (8.7%), and Jalisco (8.3%). These are not coincidences. They are the same states that began sending workers north under the Bracero Program in the 1940s. Three generations later, the financial bridge those workers built is still standing, and now it is digital, instant, and 99.1% electronic.

The Math of Sending Money to Mexico

The most accurate portrait of someone sending money to Mexico is not a generic “immigrant.” It is a 38-year-old woman who has lived in the United States for 14 years. She has two jobs: one with a paycheck and another that runs on weekends and holidays. She has a U.S.-born daughter in third grade, and a mother in Apatzingán who needs medication for diabetes. She speaks English at work and Spanish at home. She files taxes every April, even though her status is complicated. She has not seen her mother in person since 2018.

Her math is not the same as the math the news talks about. Her math is: rent ($1,400), utilities ($180), groceries ($600), her daughter’s after-school program ($200), her own phone and gas ($150), the credit card she keeps current because her credit score is the only formal financial document she has built ($120). And then, before anything for herself, $400 to Mexico. She is not “sending half her paycheck home.” She is running a household on two continents with a single budget. The remittance is not generous. It is structural.

And it is not always the same person every time. In Mexican-American families, the role of “the one who sends” rotates. The aunt sends in May, before Mother’s Day. The cousin sends in August, when school starts. The brother sends in December, when the aguinaldo bonus is short and there is a quinceañera coming. This is not random; it is choreography. It is the unspoken family agreement that no one will be the only one carrying the weight, and no month in Mexico will go by without something arriving.

What “Mandar Dinero a Casa” Actually Means

There is a specific phrase in Spanish that does not translate cleanly: mandar dinero a casa. The closest English equivalent is sending money to Mexico, but the Spanish phrase is heavier. It is not “wiring funds.” It is not “supporting family.” The word casa is doing a lot of work there. It means the physical house your mother lives in, yes. But it also means the version of you that still lives there: the daughter who left at 19, the son who promised he would come back in two years, the cousin who said the next visit would be at Christmas. Casa is the version of yourself you mailed back, payment by payment, while you stayed up here building a different life.

This is why the moment of sending is rarely just a transaction. It is the small ritual of opening the app while you are eating dinner, sending the screenshot to your sister, calling your mom 20 minutes later to make sure it landed, hearing her voice say “ya está, mija, gracias.” That sequence happens 13.7 million times a year. It is the most-repeated act of love in the Americas, and almost no economist has ever measured it.

The Calendar of the Mexican Diaspora

The Mexican remittance year has a rhythm. Anyone who has worked in money transfer can recite it from memory.

Late April and early May. The Mother’s Day surge. Día de las Madres in Mexico is May 10, and it is a national event of a different intensity than in the United States. Flowers, mariachi serenades at 6 a.m., a real meal, sometimes a small piece of jewelry. The transfers in late April are often $50 or $100 above what a sender normally moves: that is the bouquet, the cake, the manicure, the things the sender wants their mother to have without having to ask.

August. Back to school. The school year in Mexico starts in mid-August, and the cost of uniforms, shoes, books, and that one specific notebook the teacher demanded falls heavily on grandmothers raising grandchildren whose parents are abroad. The August spike in remittances is so consistent that the Bank of Mexico tracks it as a seasonal pattern.

September 16. Mexican Independence Day. El Grito. This is less about money and more about presence. Many senders schedule a video call timed for 11 p.m. Mexico time, when the president gives the Grito from the National Palace balcony. The sender stands in their kitchen in Phoenix or Brooklyn and shouts “¡Viva México!” into the phone alongside an entire family in Zacatecas. The dollar that paid for the data plan that made that call possible is itself a kind of remittance.

December. The biggest month. Christmas, Posadas, Navidad, Año Nuevo, the Three Kings on January 6. December remittances are roughly 15% above the annual average. Some of it is for gifts. Some is for the tamales that an entire neighborhood will eat on Nochebuena. Some is for the bus ticket that brings a cousin from Mexico City back to the family ranch in Hidalgo for one week. December is when the diaspora pretends, hard, that the distance is smaller than it actually is.

And the rest of the year is the steady current beneath all of it: the rent for grandma’s casita in San Luis Potosí, the cousin’s college fees in Morelia, the medication bill from the IMSS clinic, the new roof after the rain, the phone plan that lets the kid in Oaxaca call his dad in San Diego on a Wednesday for no reason.

2025 Was Hard. The Bond Did Not Break.

2025 was the first year since 2009 that Mexican remittances declined. Total flows dropped 4.6% to $61.8 billion. The U.S. share fell by $2.5 billion. Analysts at FXC Intelligence attributed the decline to three forces working together: a weaker U.S. labor market in construction and hospitality, a stronger Mexican peso that made every dollar buy fewer pesos, and the increased deportation activity of the new administration.

What is striking, though, is how small that 4.6% drop actually is. The diaspora was rocked by deportations in real numbers, by inflation that ate into discretionary income, by tax pressure on cash-based providers, and by a peso that climbed 12% in a single year. And it still moved $61.8 billion. The senders absorbed the shock. They worked an extra Saturday. They moved from cash pickup to direct deposit to save fees. They moved from Western Union to digital apps to save the spread. They became more sophisticated, more frugal, more strategic. But they did not stop.

That is the part of the story that does not make it into macroeconomic headlines. The headline is “remittances down 4.6%.” The reality is a 38-year-old woman in Riverside who picked up a fourth shift on Sundays so she could keep her mother’s medicine arriving on the first of every month, regardless of the peso, regardless of the news.

The 1% Excise Tax: A New Variable in 2026

One thing changed in January 2026 that almost no one outside the industry noticed: the federal government began applying a 1% excise tax on cash-based remittances, as part of the OBBB Act. Cash transactions, money orders, and physical wire transfers from a corner store all carry an extra 1% on top of whatever fee the provider charges. Digital, account-funded transfers (debit, ACH, app-to-bank) are exempt.

For a family sending $400 a month, that is an extra $48 a year if they send via cash, and $0 if they send digitally. Multiply that by 13.7 million transactions and the math gets serious. The tax is, in practice, a quiet policy push toward digital transfers, and the diaspora has noticed. Apps that connect a U.S. bank account to a Mexican beneficiary, like ShareMoney, have grown precisely because they are exempt from the tax and because the exchange rate they offer is closer to the interbank rate than what cash agents typically post on the wall.

Where the Money Actually Goes

When economists ask what remittances are spent on, they get one answer. When the receiving families are asked the same question, they give a different one. The economist’s answer is consumption smoothing and investment in human capital. The family answer is concrete: the medicine for grandma’s diabetes, the kid’s school uniform, the down payment on the brick house that replaced the lamina roof, the funeral for the uncle who died too young, the wedding of the prima who fell in love with someone from the next town over. Sending money to Mexico is not a single act with a single purpose; it is a thousand small obligations met one transfer at a time.

And then there is the part that no statistic captures: the small business that opened because three siblings each sent $200 a month for two years to seed it. The taxi that became a small fleet. The bakery that started in a kitchen and now employs four people. Roughly 70% of remittances are still spent on basic consumption (food, healthcare, education, housing improvements), but a meaningful 10-15% goes into productive investment: small commerce, agriculture, livestock, taxi licenses. That is how a town in Guanajuato whose grandkids all live in Atlanta still has a functioning economy. The diaspora is not just sustaining the village; it is rebuilding it.

The Bicultural Identity of Sending

Sending money to Mexico is one of the most reliable expressions of bicultural identity that a Mexican-American can perform. It is, simultaneously, a practical economic act and a cultural assertion: I am here, I am working, I am not forgetting. For first-generation immigrants, sending is an extension of familismo: the deeply rooted Mexican value that family obligation is structural, not optional. For the second generation, sending often becomes more selective and more emotional: the U.S.-born daughter who sends $100 to her grandmother every birthday, even though the grandmother has never asked for it, even though her own mother insists it is unnecessary.

This is the Mexican-American identity in motion: the high school senior in Bakersfield who has never lived in Mexico but knows exactly how much a kilo of Oaxacan cheese costs at the corner store in his grandmother’s pueblo, because his mother has been buying it remotely for fifteen years. The line cook in Brooklyn who has memorized the closing time of the BBVA branch in Apatzingán. The construction supervisor in Charlotte who knows that wires sent before 4 p.m. on Friday will land in time for his sister’s quinceañera Saturday morning. These are not statistics. These are people who have built a parallel economy of love and obligation, and they have built it with $400 transfers, one at a time.

Why the App You Use Matters More Than You Think

Here is the practical part. The choice of how you send matters, because over a decade of $400 monthly transfers, the difference between a 1.5% spread and a 4% spread is more than $1,000 a year. That is a quinceañera dress. That is a year of school supplies for two kids. That is a roof.

If your priority is speed and your relative has a debit card or a CLABE, a digital app that deposits directly into a Mexican bank account beats every cash service on price and arrival time. If your relative is in a small town in Hidalgo without a nearby bank, a service with a wide cash pickup network at OXXO, Banco Azteca, Bancoppel, or BBVA branches makes the difference between a one-hour walk and a four-hour bus ride. Most senders end up using both: digital direct-deposit for the regular monthly transfer, cash pickup for the surprise birthday or the emergency.

You can read more about each option in our corridor guides: the complete guide to sending money to Mexico from the U.S., the cluster on sending to BBVA Bancomer accounts, the workflow for Banco Azteca recipients, the convenience of cash pickup at OXXO and other retail points, and the USD to MXN exchange rate guide for timing your transfer.

A Final Word for the People Who Send

Every year, on the second Sunday of May, an entire country wakes up to bouquets that arrived from another country. Every August, a quarter of a million school supplies are bought in Michoacán and Jalisco with money that crossed the border the week before. Every December, three generations of one family eat tamales that exist because someone in Indiana picked up an extra shift in November. This is the macroeconomic story of Mexican remittances, and it is also the most personal story in North America.

If you are the person who sends, the work you do is not invisible. It is measured by the World Bank, tracked by the Bank of Mexico, studied by economists at BBVA Research and the Baker Institute, and felt in 1.6 million Mexican households every single month. But more importantly, it is felt by the specific person who picks up the phone when your transfer notification arrives. Sending money to Mexico is, in the end, the closest thing to crossing the border yourself, repeated as often as your love demands.

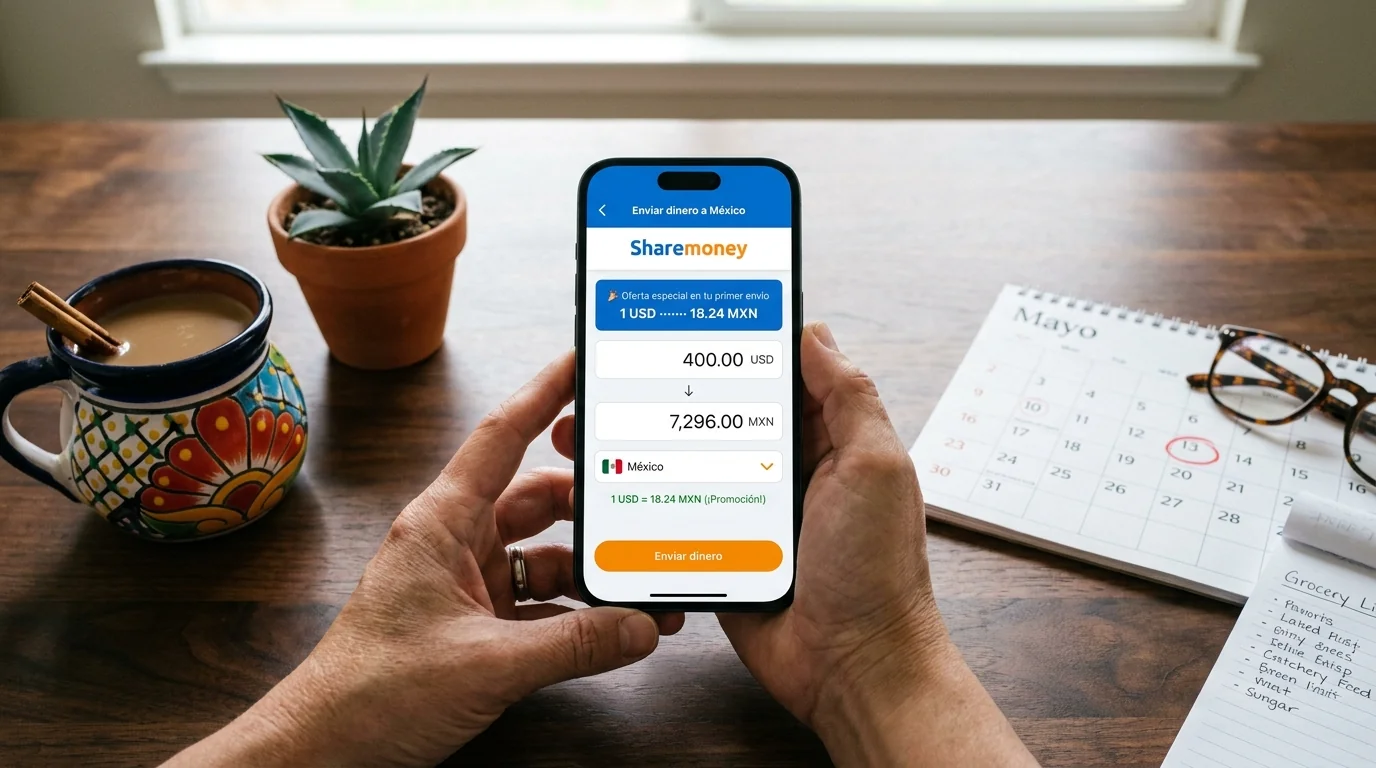

Get the Real Value of Sending Money to Mexico with ShareMoney

Our exchange rate is closer to the interbank rate than what most cash agents post. Account-funded transfers are exempt from the 1% federal excise tax. Direct deposit to BBVA, Banco Azteca, Bancoppel, Banamex, Santander, and most major Mexican banks lands in minutes. Cash pickup at thousands of OXXO, Banco Azteca, Bancoppel, and BBVA branches when your family needs it that way. The first transfer is free for new senders.

Related reading: How to Send Money to Mexico from the US: Best 2026 Guide · Send Money to BBVA Bancomer from the USA